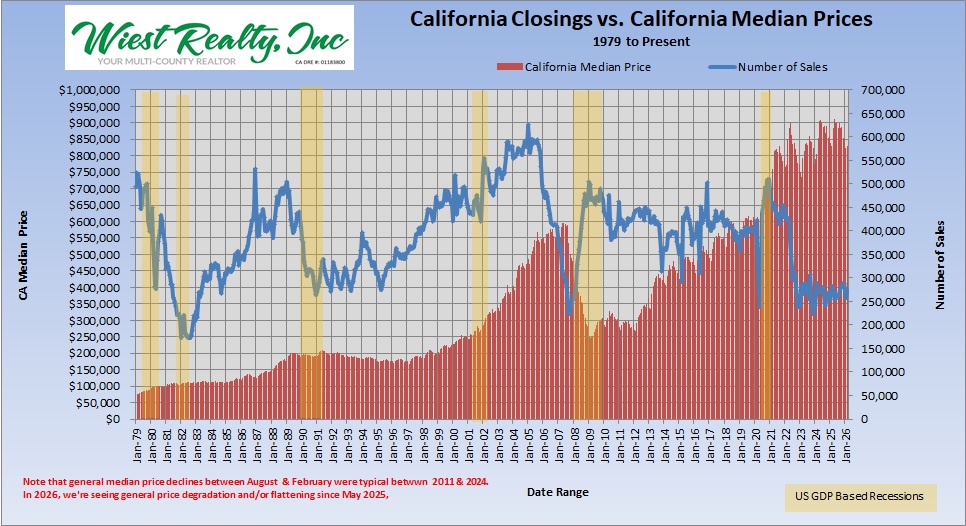

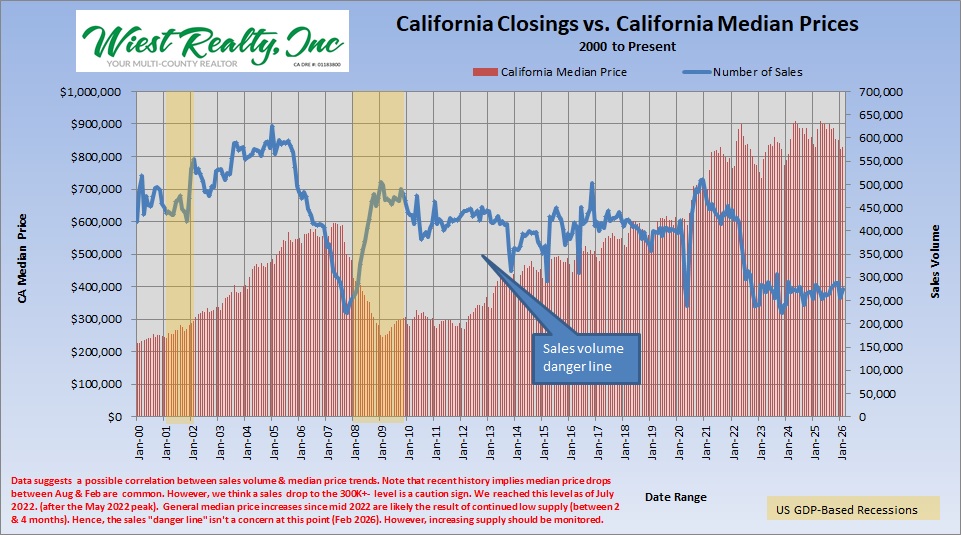

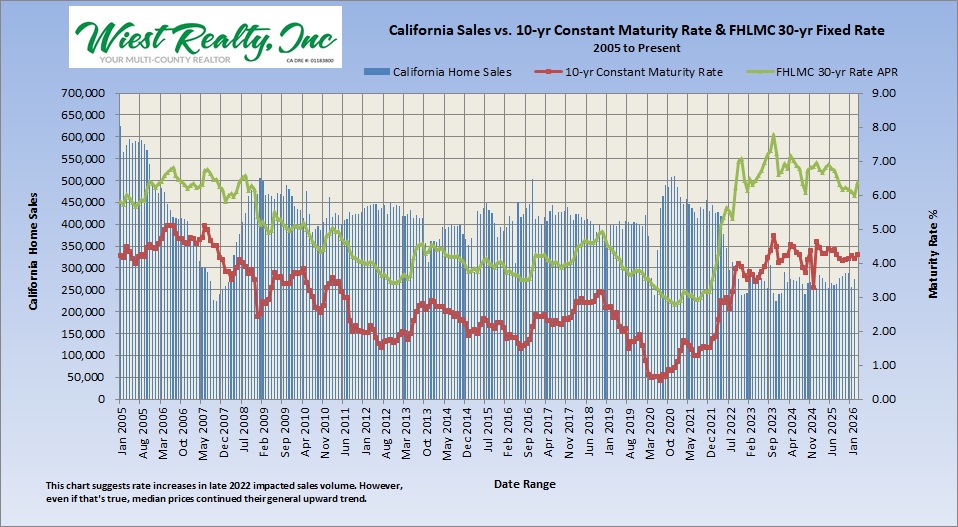

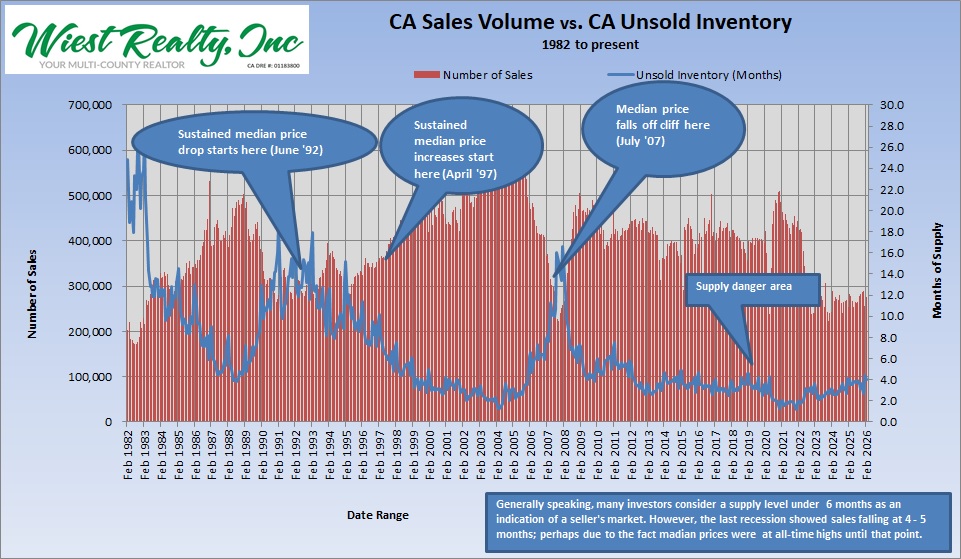

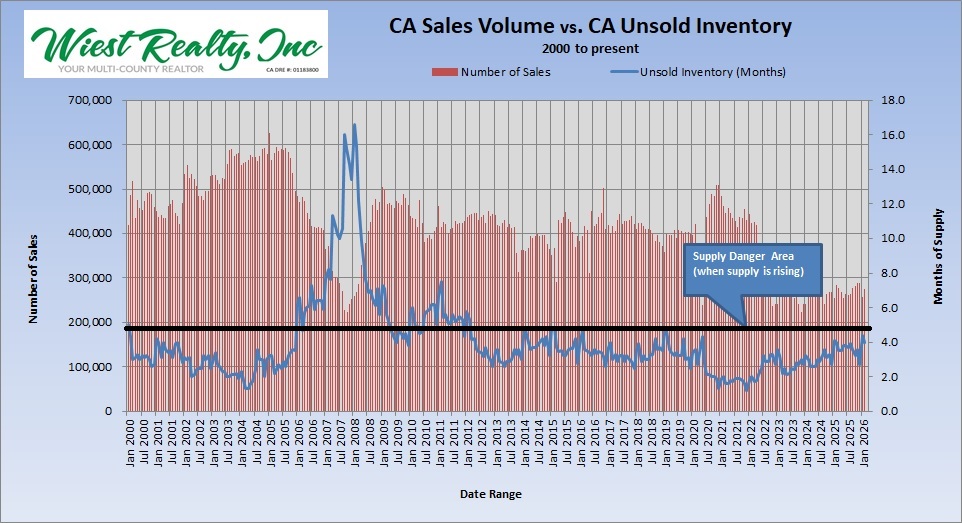

February 2026 year over year sales decreased 3.1%. Between January 2025 and February 2026, year-over-year sales numbers were positive for eight of the last fourteen months.

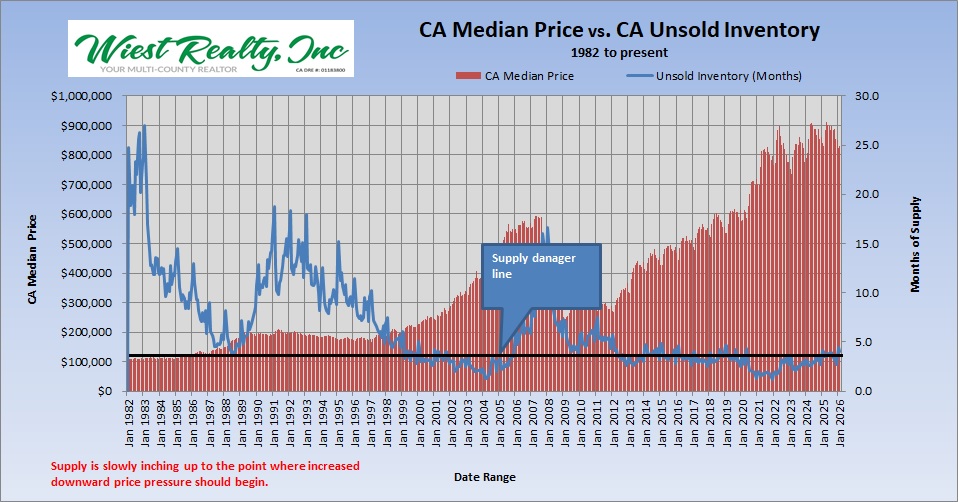

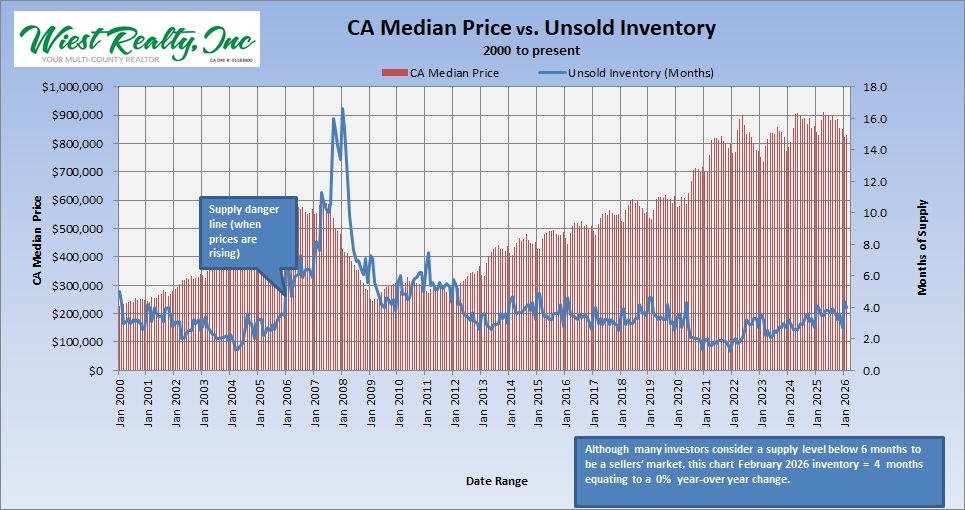

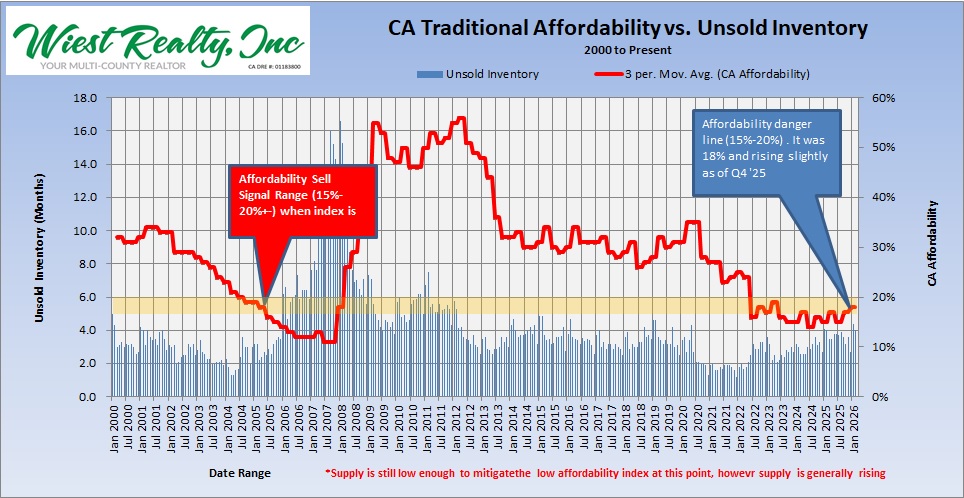

California single family home supply (unsold inventory) for February 2026 was reported at 4.0 months resulting in a 0% year over year change, Supply has been bouncing between 3.7 and 4.3+- months since January 2025. That’s notably higher than the 2024 range of 2.6 to 3.6 months. So far, however, supply is below what we call the “danger line” but keep an eye out for more median price softness once supply starts pushing the 4.5 to 5 month area.

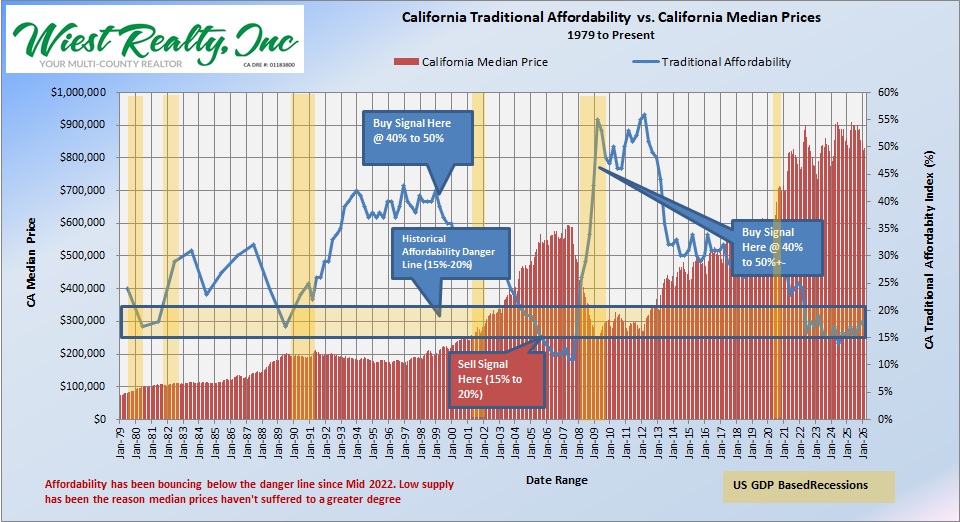

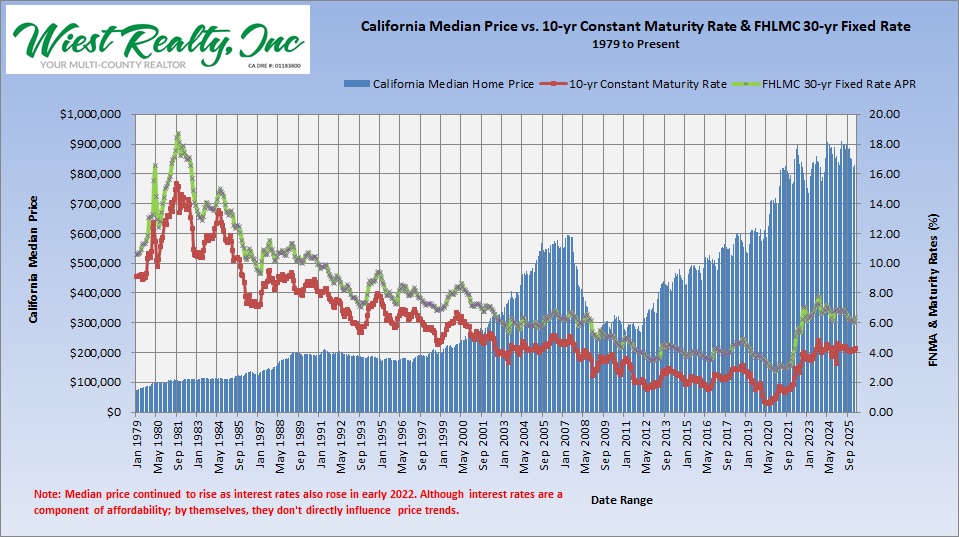

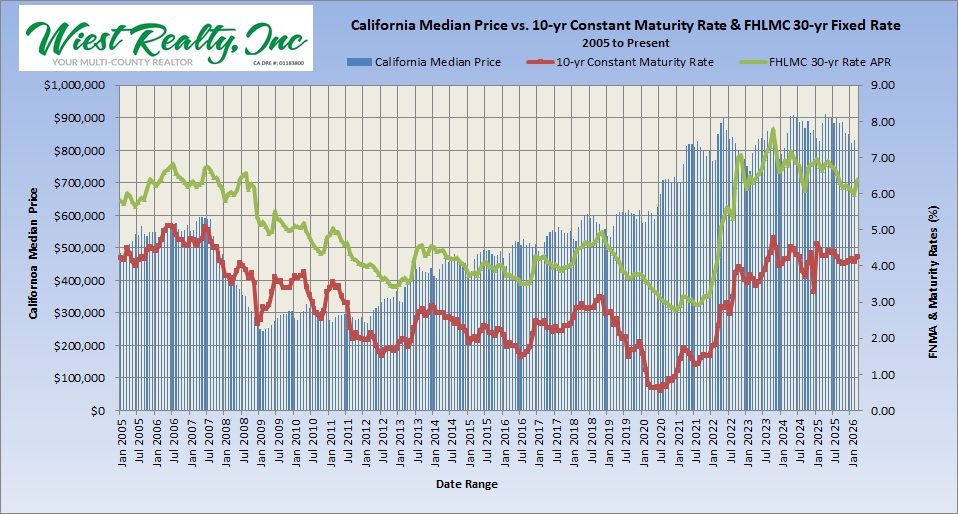

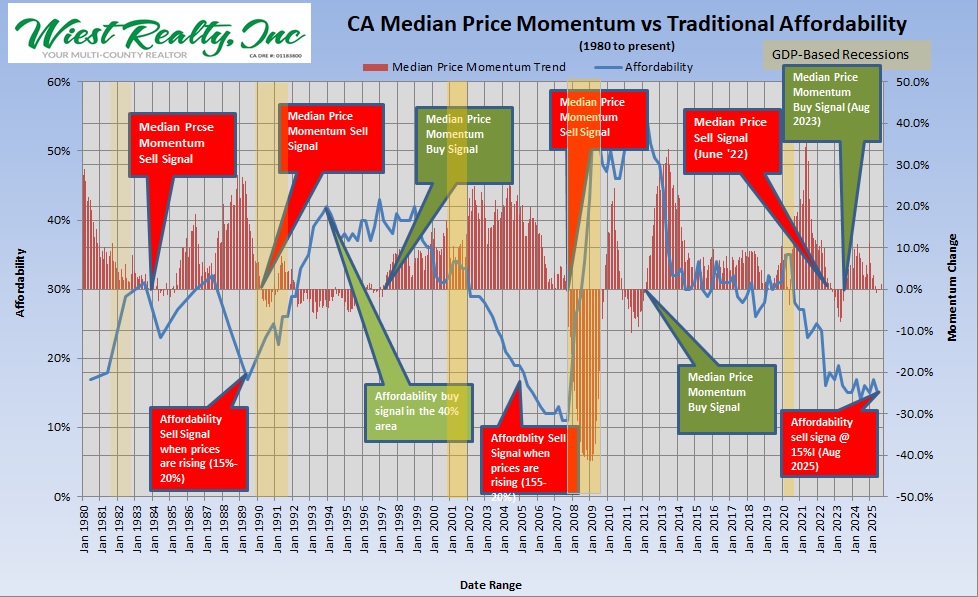

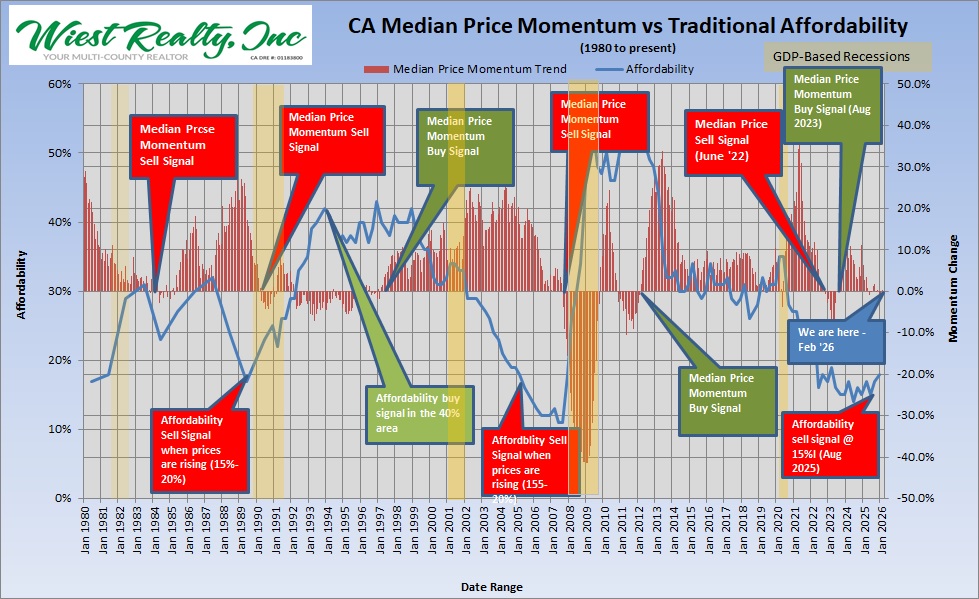

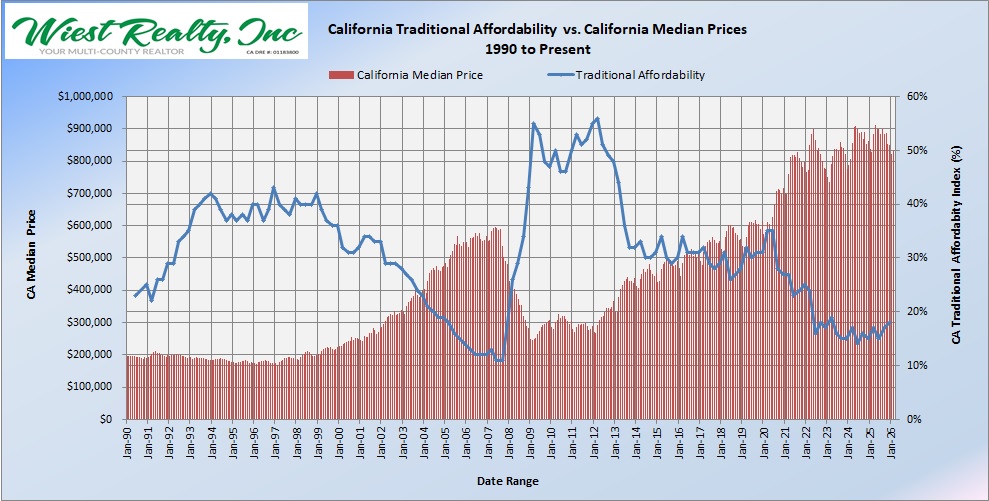

With the California Q4 ’25 traditional affordability index at 18%, one would expect some price damage – and that’s what we saw throughout the last half of 2025. Year-over-year median price momentum crossed into negative territory in May 2025.. Historically (since 2011), median California prices tend to generally drop between August and February. So, the slight February 2026 median price increase of 0.9% is not much of a surprise.

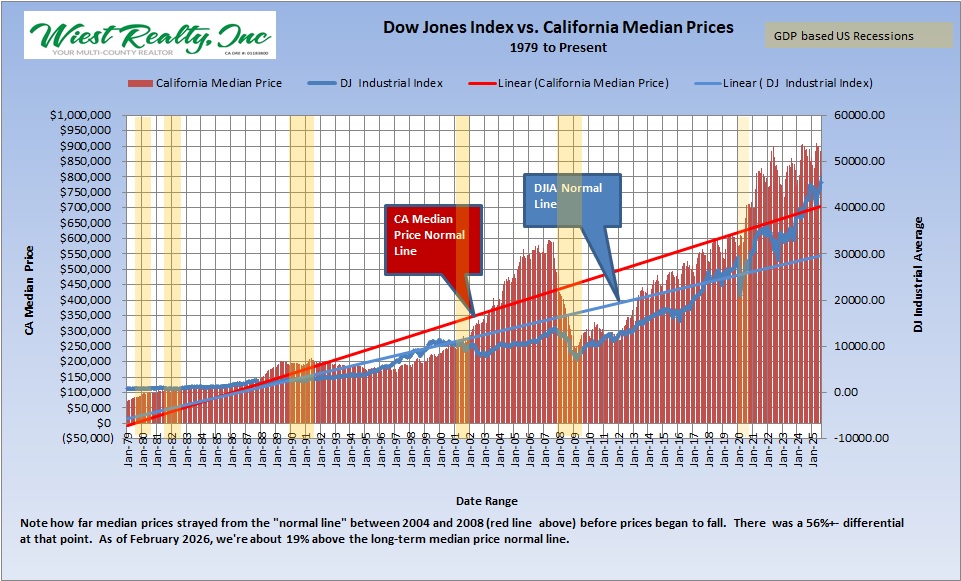

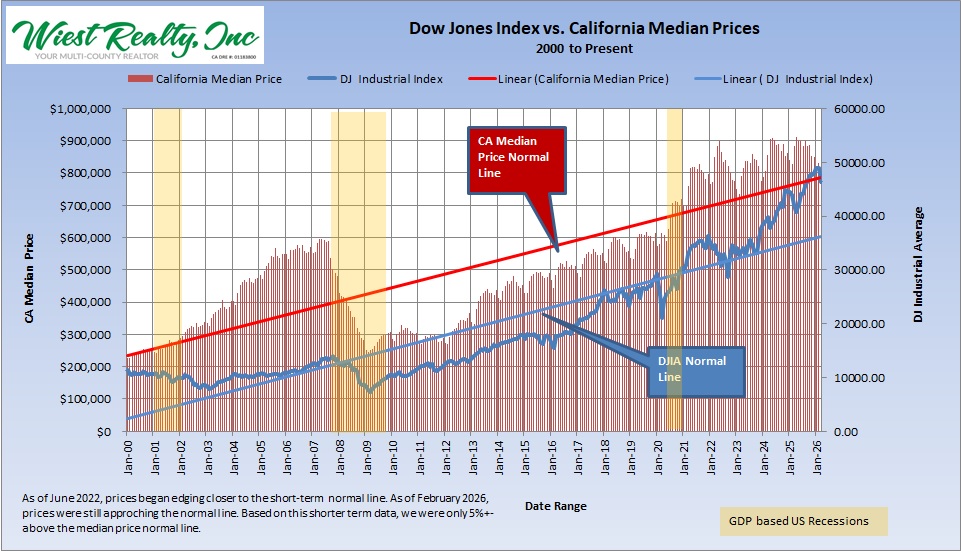

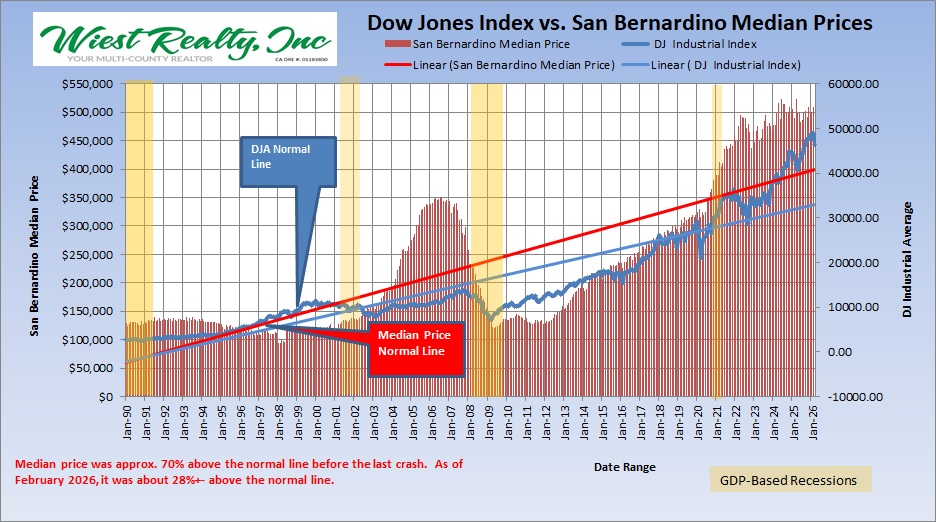

Median California single family home prices for 2026 ticked upward between January and February about 0.9% thereby equating to a 0.2% year over year increase. Note, however, median price is getting closer to the “normal line” (a linear track that centers the distribution of median prices). The long-term normal line shows a deviation of about 19% as of February 2026 with the short-term line showing only about 5%. These numbers along with median price momentum bouncing between small positive and negative territory implies continued price damage is likely on the state level overall.

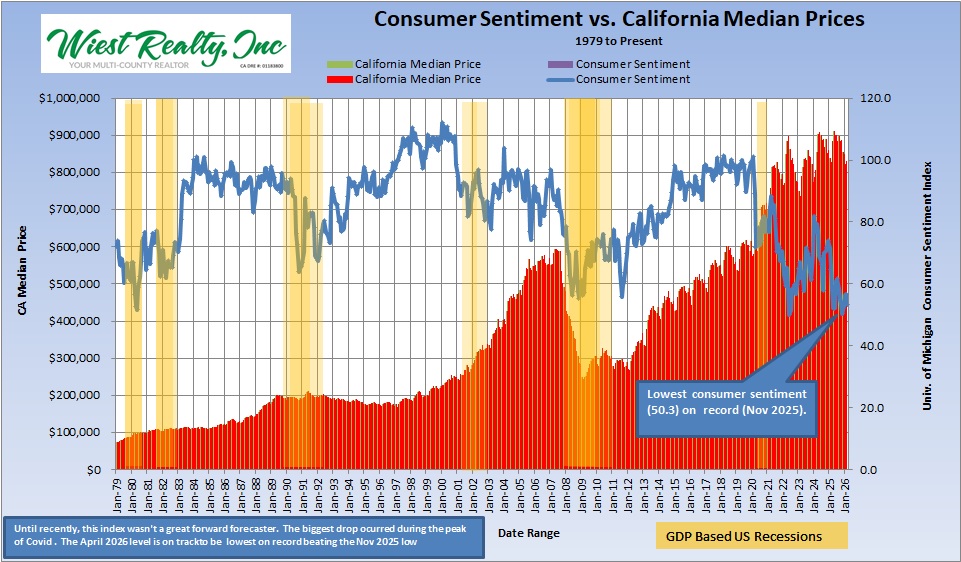

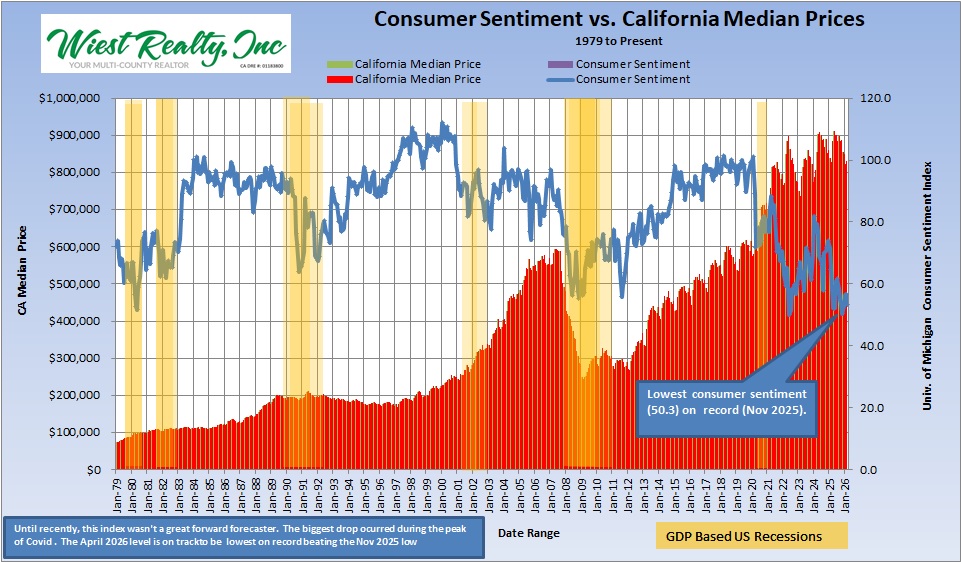

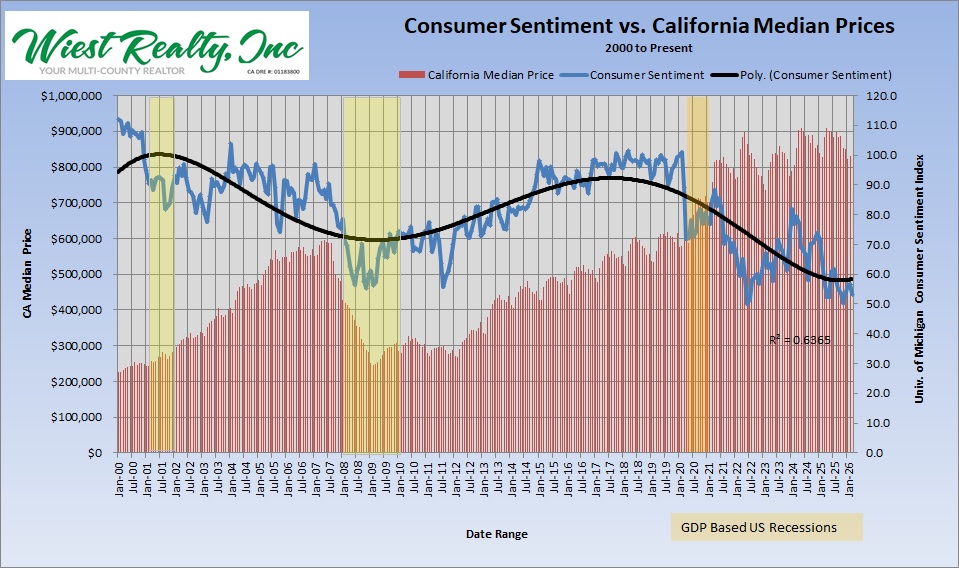

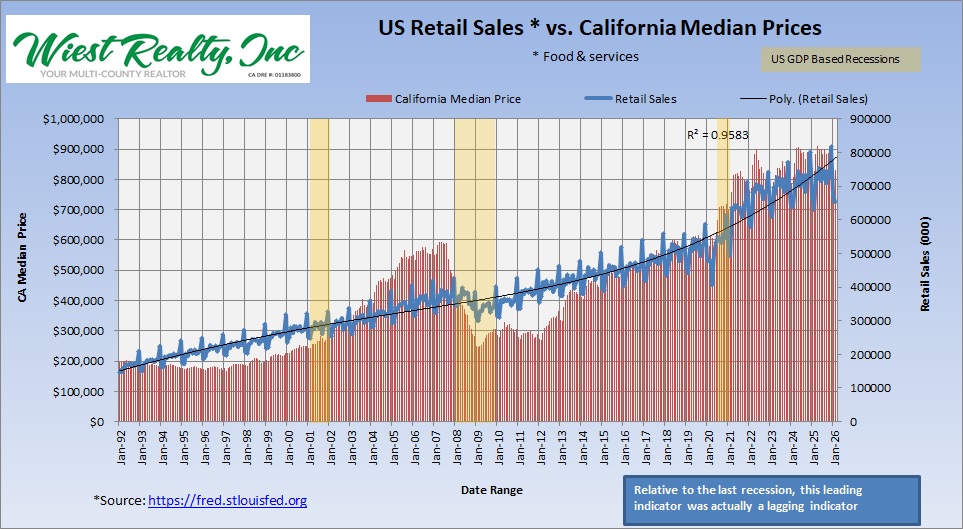

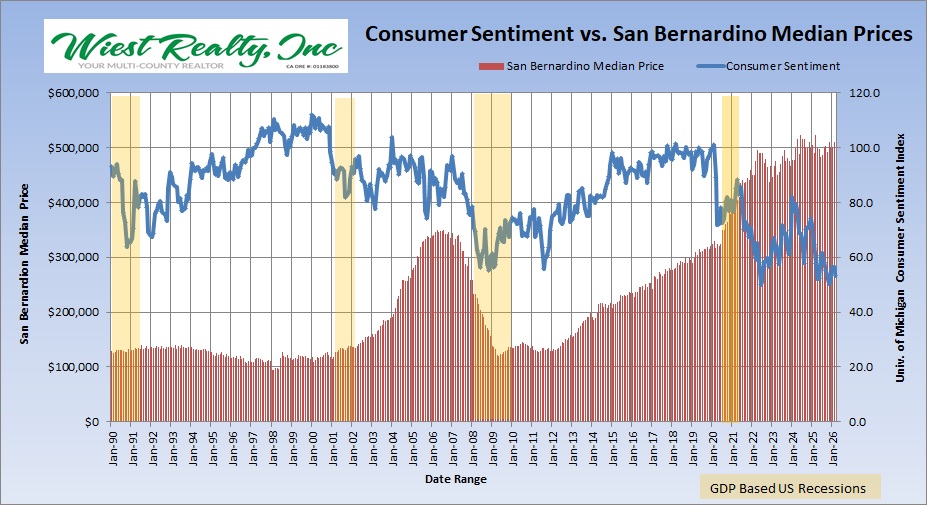

Consumer Sentiment continues its general decline. While this index is considered a leading indicator, it doesn’t lead by much. However, it suggests more down-side risk should be considered in your investment models.

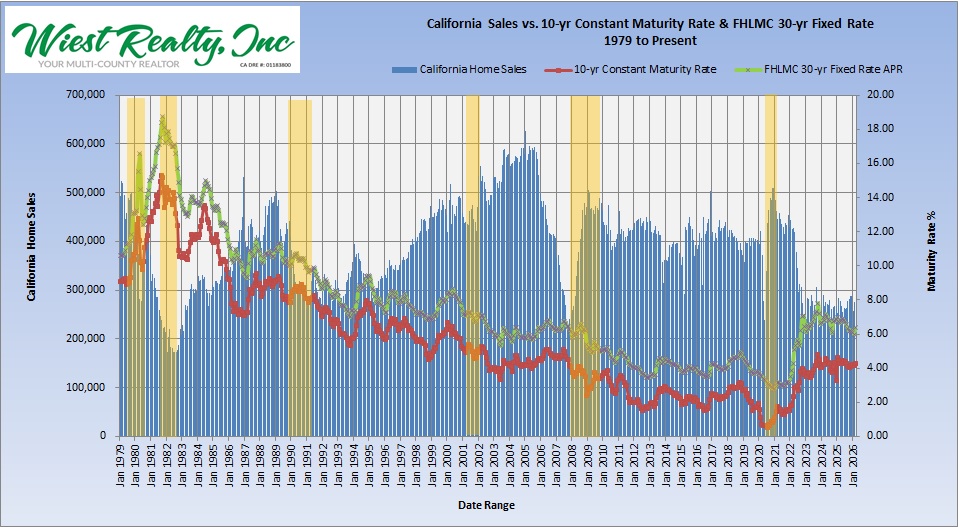

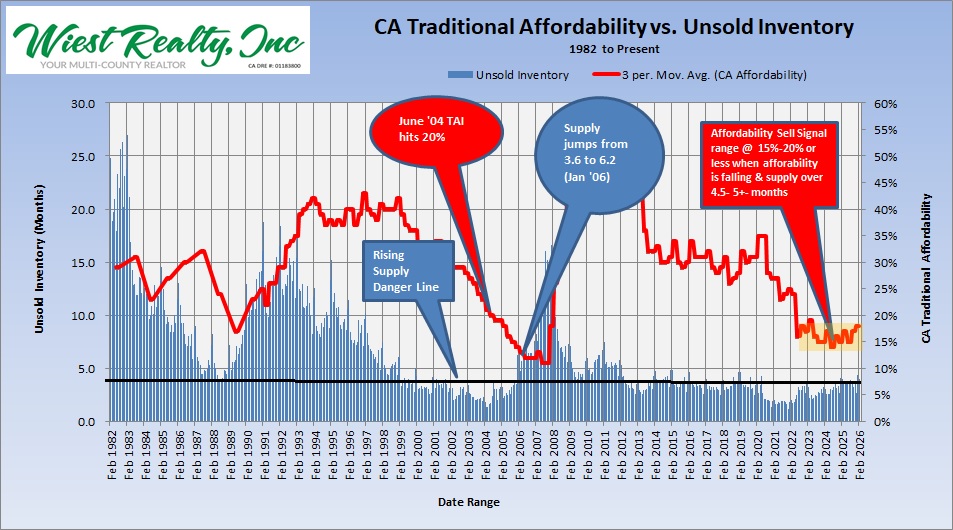

People are still not willing to give up those 4% or less mortgages to move up to a larger home. Per Redfin Data, about 55% of US mortgages carry a note rate of 4% or less. California data estimates are 77% of mortgages are under 4.25%. This is probably one factor mitigating supply increases. Hence, supply remains relatively low. In fact, California supply has been generally around or under 4 months for 10+- years. However, keep an eye on supply as it is increasing and will likely impact median prices. Of course there are many external factors that can influence trends. So assuming no wars, gas shortages, political upheaval, major population exodus, or similar incidents , it’s our opinion that if supply starts pushing the 5-month level and traditional affordability stays in the 18% area, we will see increased median price degradation. Check out the charts and tell us what you think.

The following data applies to California as a whole and applies only to single family dwellings. Every local market is different. If you need help with your local market, simply call us or fill out the contact page.

Check out our momentum indicators page for the latest trends.

Check out the graphs – let us know your opinion.